Questions about the Palms Acquisition

When will Red Rock disclose the Palms purchase agreement?

Since the May 10 press release announcing the acquisition, Red Rock has not filed the definitive purchase agreement with the SEC yet. Investors should be able to review and evaluate the details of this significant transaction, which, at $312.5 million, cost nearly 70% of the company’s 2015 Adjusted EBITDA ($451 million) and is expected to be financed with new debt.

What will Red Rock have to do to bump up Palms’ EBITDA by 25% in one year?

Back in May, Red Rock management stated that they expect the Palms to generate “over $35 million” in EBITDA in the first full year of ownership by Red Rock. At the same time, they say the property’s EBITDA run rate is at “approximately 60% below its peak level.”

The Palms reportedly had EBITDA of about $70 million before the Great Recession, according to Debtwire/Financial Times. If one assumes that was the peak, then “60% below peak” would imply current annual EBITDA of about $28 million. Will Red Rock be able to expand Palms’ EBITDA by 25% (to $35 million) during its first full year of ownership? What kind of revenue growth and/or cost cutting will be required to achieve such a large increase in EBITDA in one year?

Will “Palms Station” cannibalize Palace Station?

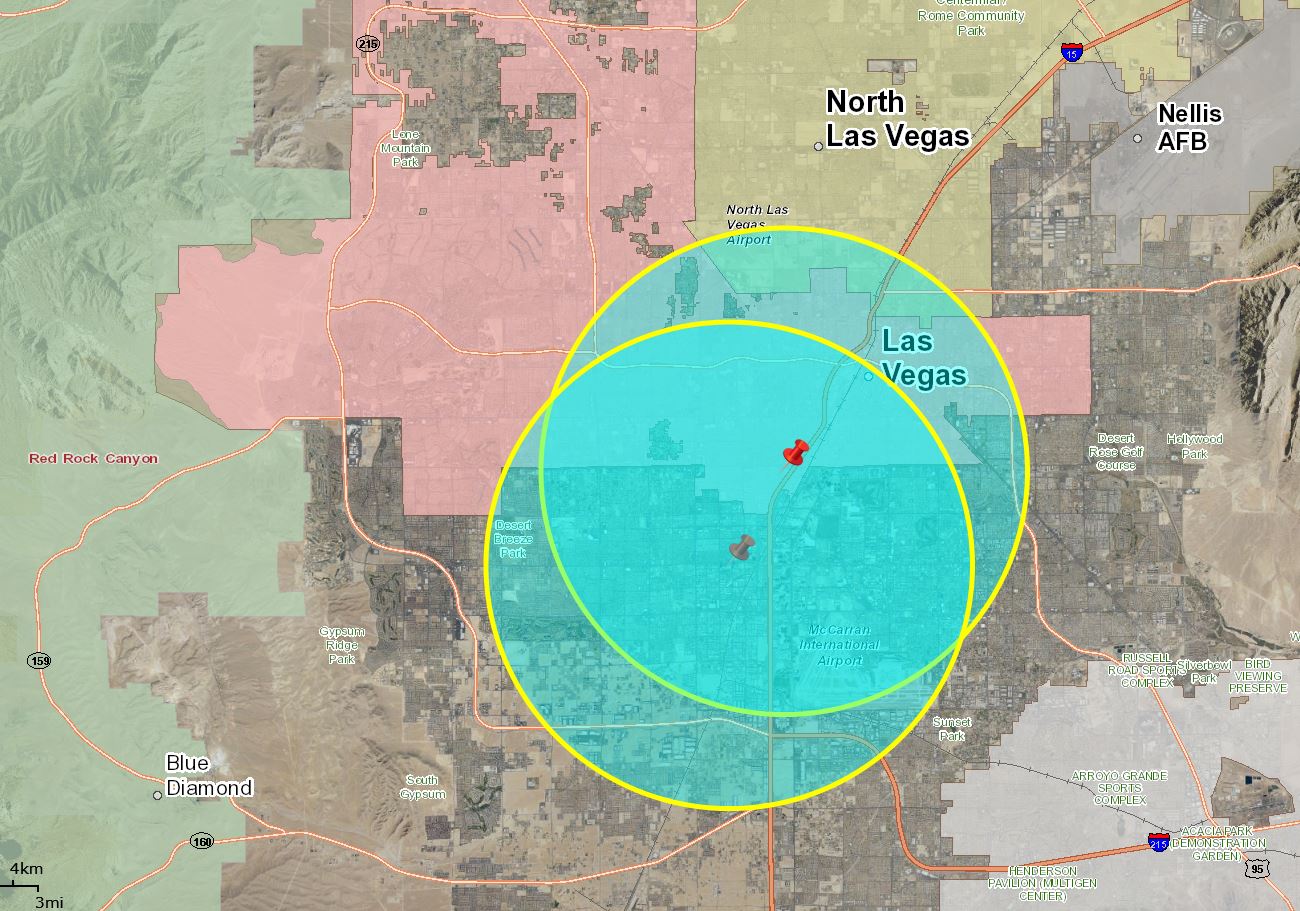

Also back in May, Red Rock management described Palms as being “located in one of our most underpenetrated areas in the Las Vegas Valley from a boarding pass member standpoint.”

But the Palms is only 2.3 miles away from Red Rock’s Palace Station, and if you draw a five-mile-radius circle around each of these two properties, there is a 71% overlap between the two circles. How will the company ensure that its efforts to grow the business of Palms will not come at the expense of Palace Station?