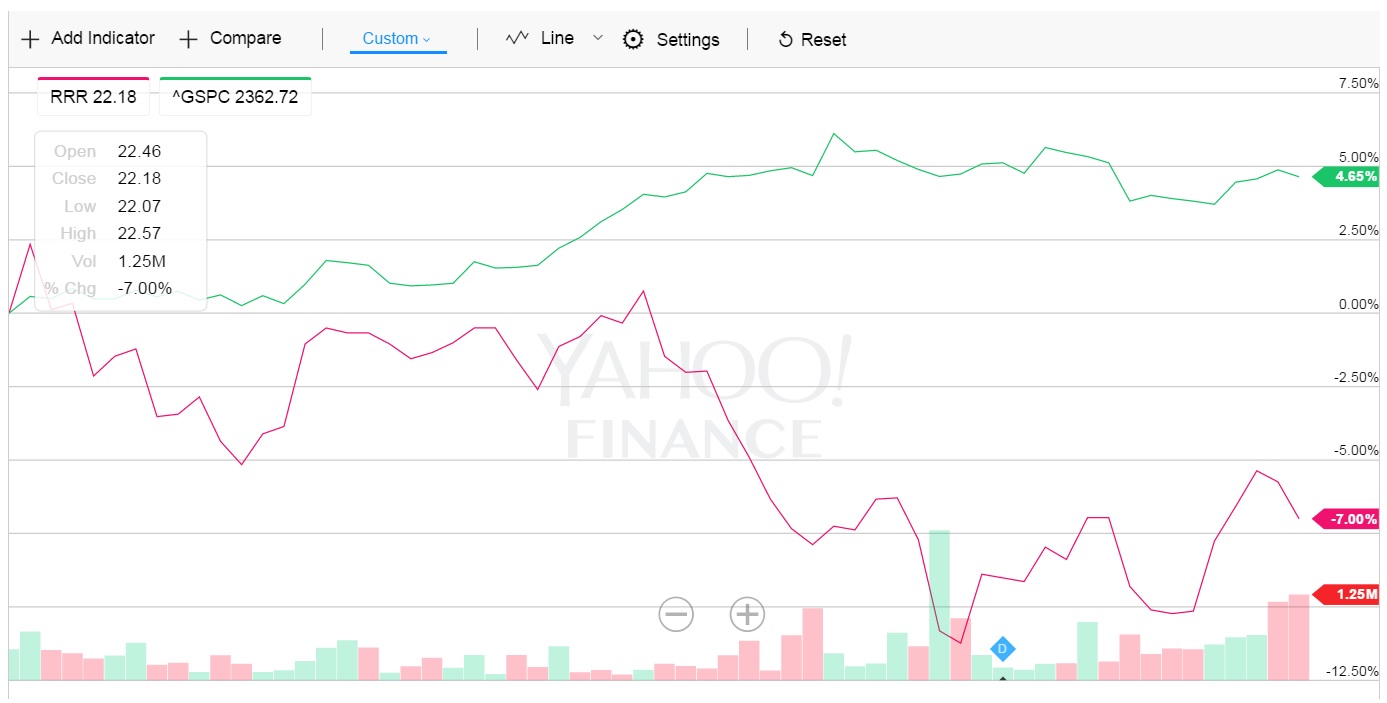

New Costs to Pressure Margins at Station Casinos

In December, Station Casinos announced a company-wide new benefits package, immediately after the National Labor Relations Board (NLRB) announced there was going to be a union election at the company’s flagship Red Rock Casino. We estimate the new benefits would add nearly $70 million in operating costs on an annual basis, or a 400-bps hit to the EBITDA margin at the company’s Las Vegas operations, which had a 25.9% margin in 2019 ($454.8 million in adjusted EBITDA over $1.76 billion in net revenues).[1] Our estimate includes only the costs of the new free HMO plan with family coverage and no deductibles and a new 401(k) program with direct employer contributions (see Appendix 2).

Station Casinos took on these higher costs even as it continues to lose operational flexibility with respect to labor cost as a result of a series of union elections since 2016. Employees have voted – sometimes overwhelmingly – to unionize through NLRB elections (for example, 67% for the Culinary and Bartenders Unions at Boulder Station, 78% at Green Valley Ranch, 82% at Sunset Station, 83% at the Palms, and 85% at Fiesta Rancho), and the company – the operating subsidiary of Red Rock Resorts, Inc. – is now legally required to collectively bargain over working conditions, including benefits, at its casino hotels where unions are negotiating for a contract. Local affiliates of Operating Engineers and Teamsters have also won union elections at various Station properties, creating legal bargaining obligations for the employer. The company cannot unilaterally take away the new benefits it now provides where it has an obligation to bargain. And it is hard to see management try to reduce benefits only at non-unionized properties without creating significant issues among the workforce.

In the past, Station Casinos was able to take away or change benefits at will. For example, between 2008 and 2016, the annual employee premium for the company’s HMO plan went from zero to $420 for individual coverage and from $1,080 to $3,000 for family coverage. It also “suspended” its 401(k) matching contributions in December, 2008, and didn’t restore the match until 2012.[2] Station Casinos cannot make such unilateral changes anymore at its unionized properties without negotiating with the representative union. The new benefits and their higher costs can therefore become more or less locked in even without a settled union contract.

It is also worth noting that Station Casinos has been an outlier in the Las Vegas gaming industry in not participating in the cost-effective multi-employer union health plan of the Culinary and Bartenders Unions, which provides a premium-free, no-deductible PPO family coverage plan. Healthcare costs are rising fast for Station Casinos, even before the most recent improvement in benefits (expanded no-premium family coverage no more deductible for its HMO). Other large casino operators in Las Vegas (including MGM, Caesars, Wynn, Boyd Gaming, Penn National, Golden Entertainment) have seen more modest increases in what they pay to provide good healthcare for their unionized employees under the multi-employer union health plan. Station Casinos’ own health insurance plan cost, on a per covered person basis, increased by 37.5% from 2013 to 2018.[3] In contrast, the required employer contribution rate for the union health plan only increased by 10% over the same period.

Station Casinos investors should ask management why the company would rather unilaterally raise labor costs instead of agreeing to participate through a collective bargaining agreement in the cost-effective multi-employer union health plan and other union benefit plans. After all, it is not management’s own money that is going out of the company’s coffers to pay for these escalating costs.

Appendix 1: The new benefits package at Station Casinos

- Starting in January this year, employees making less than $41,600 in annual salary or $20.00 per hour will be eligible for a premium-free HMO health plan, even with family coverage. Previously, an employee would have to pay $780 a year to get family coverage on the company’s HMO plan.

- Also, the company eliminated deductibles for employees enrolled in its HMO plan. Previously, the company’s HMO plan had a $500 annual deductible for those with individual coverage and $1,000 deductible for those with family coverage.

- The company will open three on-site “medical centers” at Red Rock Casino, Sunset Station, and Texas Station or Santa Fe Station. These centers will provide “free medical provider visits”, “free generic drugs”, “free lab work”, and fast appointments”. The Culinary Health Fund – the multi-employer health plan for Culinary and Bartenders union members and their families – had opened its own health center in 2017 at a cost of $30 million.

- Station Casinos also now offers a “unique and expanded” 401(k) plan. For those with 1 to 24 years of service, the company will contribute $0.50 per hour worked into their 401(k) accounts. For those with 25 years or more of years of service, the company will contribute $1.00 per hour worked. It is not clear how this new scheme of nonelective contributions[4] will work alongside the company’s “traditional” 401(k) plan, which provides for a matching contribution of 50% of the first 4% of a participant’s own contributions.

- The company also announced “new training programs”, “Team Member recognition program”, “fast hiring”, and a new attendance policy.

Appendix 2: The cost of the new benefits package at Stations Casinos

In 2018, Station Casinos paid $62.7 million for its HMO and PPO contract with its health insurance provider. The cost would have likely increased for 2020 even if the company had made no changes. With the changes:

- No premiums for HMO family coverage: We estimate about 40% of the workforce would choose to enroll in the free HMO with family coverage and about 17% of the workforce would choose free HMO with individual coverage. Based on Kaiser Family Foundation data, the average annual premium cost of an employer-sponsor health plan was $18,357 for family coverage and $6,032 for individual coverage in 2018. We estimate Station Casinos would pay at least $112.2 million in annual premiums for its new HMO plan.

- No deductible: The company HMO plan had a $500 annual deductible for individual coverage and $1,000 for family coverage. If the company pays these on behalf of the participants, the total would be approximately $6.7 million.

- We therefore estimated the cost of the new HMO plan to be about $118.9 million, or $56.3 million more than the 2018 cost of $62.7 million.

The employer contributions under the new 401(k) program can be estimated as follows:

- We estimate that 90% of the workforce of 14,000 have more than 1 and fewer than 25 years of service and will receive $0.50 per hour worked under the new 401(k) program.

- We estimate that 5% of the workforce have more than 25 years of service and will receive $1.00 per hour worked under the new 401(k) program.

- We estimate the average number of hours worked in a year to be about 1,900. This means that the company will make about $13.3 million of new contributions a year to employees’ 401(k) accounts.

Putting the two benefits together, we therefore estimate these two new benefits alone would add approximately $69.6 million to Station Casinos’ annual payroll.

We do not have a good way to estimate the additional cost of the three new on-site medical centers or the new training and hiring initiatives announced in December.

[1] 2019 10-K, filed 2/21/2020.

[2] https://www.reviewjournal.com/news/station-casinos-suspends-matching-contributions-for-employees-retirement-plans/

[3] See the 5500 filings by Station Casinos LLC Employee Benefit Plan. In 2013, it paid $45,468,966 to cover approximately 18,407 person through its HMO-PPO-prescription drug contract with Health Plan of Nevada. In 2018, it paid $62,651,752 to cover approximately 18,440.

[4] https://www.investopedia.com/terms/n/non-electivecontribution.asp